What Is the 22.1 Disclosure? What Chicago Condo Sellers Need to Know Before Buyers Do

Illinois is one of the only states in the country with this specific condo disclosure requirement. Most Chicago condo sellers never read their own 22.1 packet before it lands in a buyer's hands. That's a problem.

Before We Go Any Further

The 22.1 disclosure is an Illinois-only, condo-only document package that sellers are legally required to provide to buyers. It contains your building's financials, reserve fund status, meeting minutes, rules, and any pending litigation. Buyers and their lenders read it closely. Most sellers never do.

What Is the 22.1 Disclosure?

Under Illinois condo disclosure law, it is named after Section 22.1 of the Illinois Condominium Property Act. That law requires every condo seller to provide the buyer with a specific set of documents from the association before the deal closes.

This is not a form you fill out. It is a packet your HOA or management company assembles. It can run anywhere from 30 to 200 pages depending on the building and what has been happening inside it.

You do not get to choose what goes in. The law dictates it. Your association sends what it sends, and buyers see all of it.

What's Actually in the Packet?

This is where sellers get blindsided. Most assume the 22.1 is just a standard disclosure form. It is not. Here is what buyers and their lenders receive:

The HOA budget. Current operating expenses, income, and how the association is managing money month to month. If you want a deeper breakdown of what those numbers actually include, here's a full explainer on HOA budget and what it covers. If the budget looks stretched or fees are about to increase, buyers will see it.

Reserve fund balance. This is the savings account for big future repairs, roofs, elevators, common area work. A healthy reserve signals a well-run building. A thin one raises red flags. In some downtown Chicago buildings, reserve studies show significant underfunding, and that information is right there in the packet.

Pending or active litigation. If your building is in a legal dispute with a contractor, a former owner, or anyone else, it is disclosed here. Lenders often will not approve financing on units in buildings with certain types of pending litigation.

Meeting minutes. Board meeting notes from the past several months. If there have been heated debates about upcoming special assessments, delinquent owners, or major repairs being deferred, it is in the minutes. Word for word.

Rules and declarations. Rental caps, pet policies, move-in and move-out procedures, and renovation restrictions.

Special assessment history. Any additional charges levied on unit owners beyond the regular monthly fee.

Insurance certificate. Coverage for the building's common areas, which affects what a buyer's lender requires them to carry separately.

Why This Is a Seller Problem, Not Just a Buyer Problem

Here is the angle that nobody writes about. Most of the content about 22.1 disclosures is written for buyers. Read the documents carefully. Watch for red flags. Review the reserves.

But sellers are the ones who need this information first.

You live in the building. You know there was a pipe issue on the 12th floor. You remember the board sent out a notice about parking garage repairs. You heard someone mention a lawsuit at the last owner meeting. But you may not know exactly what made it into the official record, how it was worded, or how a buyer's attorney is going to read it.

When a buyer's agent calls after the disclosure review and says their client is pulling out because of what they found, that is too late. The deal is dead. You are back on the market with a days-on-market counter that every future buyer will notice.

The fix is simple. Request the packet yourself before you list.

How to Get Your Building's 22.1 Packet Early

When it comes to selling a condo in Chicago, the 22.1 packet is one of the few steps sellers control entirely. In Illinois, the seller is legally entitled to request the disclosure package from the association before a buyer is ever involved.

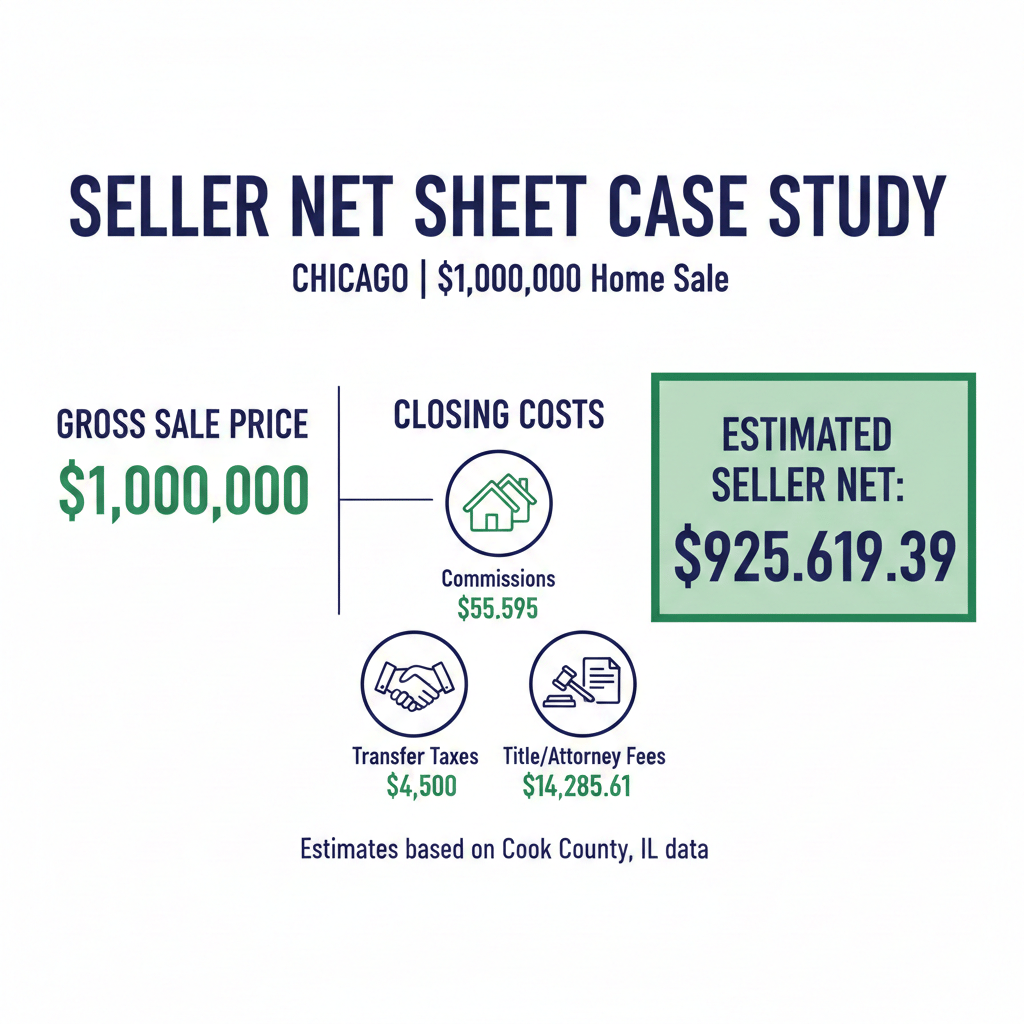

Contact your HOA management company and request the 22.1 disclosure package. Some buildings charge a fee for this, typically between $100 and $400 depending on the management company. That fee is paid whether you order it before listing or after you are under contract anyway, so there is no reason to wait.

Once you have it, read it. If you cannot, bring it to your attorney or your agent and go through it together. What you are looking for:

The reserve balance relative to the building's size and age. Is it healthy or concerning? How will a buyer interpret it?

Any active or pending litigation. Even minor disputes can slow or kill financing. Know before your buyer does.

Upcoming assessments or capital projects discussed in the minutes. If there is a rooftop replacement being planned, a buyer's lender may require reserves that do not exist.

Rental cap status. If your building is at or near its rental cap, that eliminates a large category of buyers who plan to rent the unit.

The Lender Angle Sellers Often Miss

Your buyer's lender is not just reviewing the buyer. They are reviewing your building.

For conventional loans backed by Fannie Mae or Freddie Mac, the lender must evaluate the condo project before approving financing. A building with inadequate reserves, active litigation, or a high percentage of investor-owned units can be classified as non-warrantable. In Chicago real estate, a non-warrantable condo designation means conventional financing is off the table. These are the same red flags buyers and lenders look for when evaluating any downtown Chicago building. That means the buyer cannot get conventional financing, which eliminates most buyers entirely.

This is not rare in downtown Chicago condo buildings. Buildings along Lake Shore Drive in Streeterville, high-rises in River North, and some older South Loop towers have characteristics that lenders scrutinize carefully. Sellers who know about these factors in advance can adjust pricing, target the right buyer pool, and avoid deals that fall apart in underwriting.

A buyer who cannot finance your unit is not a buyer.

What a Good 22.1 Review Looks Like Before Listing

Before you list, your 22.1 review should tell you:

The reserve fund is healthy or has a clear plan. Buyers and lenders want to see a fully funded or actively funded reserve. A low reserve does not automatically kill a deal, but it should affect your pricing strategy. For investors buying your unit as a rental, reserve fund health and special assessments are often the first numbers they run.

No active litigation that affects financing. Routine vendor disputes may be fine. Construction defect lawsuits are not.

The budget is balanced. Operating in a deficit is a red flag buyers will use to negotiate.

Meeting minutes reflect stable management. Constant board turnover, contentious votes, or deferred decisions show up in the minutes.

If any of these areas look concerning, you want to know before you price the unit, before you stage it, and before you invest in marketing.

Why Downtown Chicago Sellers Specifically Need This

Every downtown Chicago building is different. The 22.1 for a boutique 30-unit West Loop loft building looks nothing like the one for a 400-unit high-rise in Streeterville. Reserve requirements, governance structures, and the kinds of capital projects that come up vary enormously.

Christine Hancock has sold over 300 units in the West Loop alone and has reviewed hundreds of 22.1 packets across Downtown Chicago buildings including in River North, Gold Coast, South Loop, and Streeterville. The patterns she has seen are real: sellers who review the packet in advance close faster, price more accurately, and lose fewer deals in the attorney review and inspection period.

The buildings where deals fall apart most often are not the ones with the smallest units or the lowest prices. They are the ones where the seller did not know what was in the packet.

Walk Away Knowing This

- The 22.1 disclosure is an Illinois state law requirement that only applies to condo sales.

- It includes your HOA budget, reserve fund, meeting minutes, pending litigation, rules, and insurance.

- Buyers and lenders both review it closely before committing to a purchase.

- Sellers can and should request the packet before listing, not after going under contract.

- Problems found in the 22.1 that are discovered late can kill deals, delay closings, and force price reductions.

Frequently Asked Questions

What is a 22.1 disclosure in Illinois? It is a document package required under the Illinois Condominium Property Act that condo sellers must provide to buyers. It includes the building's financial records, reserve balance, meeting minutes, rules, litigation status, and insurance details.

Does the 22.1 disclosure affect my sale price? It can. If the disclosure reveals low reserves, a pending special assessment, or active litigation, buyers may negotiate a lower price or walk away. Reviewing it before listing lets you price accordingly and avoid surprises.

How long does it take to get the 22.1 packet? Most management companies turn it around in three to ten business days. Some buildings expedite for a fee. Order it early so you have time to review it with your attorney before listing.

Can a buyer back out because of the 22.1 disclosure? Yes. Illinois law gives buyers a right of rescission after receiving the 22.1 documents. They can cancel the contract within a specific window, no penalty. This is why knowing what is in the packet first is so important.

Do I have to provide the 22.1 even if I'm selling as-is? Yes. The 22.1 is a legal requirement under the Illinois Condominium Property Act and is separate from an as-is sale. It relates to the building and association, not the condition of your individual unit.

Ready to find out what your building's 22.1 packet says before your buyer does?

Call or text Christine Hancock at 312-296-9300 to talk about your unit's value, what your building's disclosure looks like, or what it would take to get you to the closing table.

Want to know what your building's disclosure actually says before buyers and lenders do?

ABOUT THE AUTHOR

Christine Hancock is a Chicago Realtor with @properties Christie's International Real Estate, bringing more than 25 years of experience and over $200 million in closed sales in the downtown condo market. With 96 five-star Zillow reviews, Christine is recognized for her commitment to client satisfaction and market expertise.

She specializes in high-rise and luxury condominium sales in West Loop, South Loop, River North, and Streeterville, helping buyers and sellers navigate complex transactions with data-driven pricing strategies and deep neighborhood insight.

Christine partners with clients to evaluate market trends, position properties competitively, and make confident, informed decisions in Chicago's vibrant downtown housing market.

Call or text 312-296-9300 to discuss current market conditions or your real estate goals.