Wondering whether you should cash out your downtown Chicago condo or hold onto it as a rental? It is a smart question, especially in a market where both buyer demand and rental demand remain active, but the math can shift quickly once you factor in HOA dues, taxes, and building rules. If you are weighing your next move, this guide will help you think through the real tradeoffs so you can make a confident, informed decision. Let’s dive in.

Downtown Chicago Conditions Matter

If you own a condo downtown, you are making this decision in a market with real activity on both sides. According to the Chicago Association of Realtors market presentation, downtown Chicago recorded about $1.2 billion in sales volume in 2025, with an average price per unit of $442,191.

That matters because it shows there is still meaningful buyer depth in the downtown condo market. At the same time, no two buildings perform exactly the same way. Your result can vary based on reserves, special assessments, monthly dues, view, floor, and even your unit’s stack within the building.

On the rental side, conditions have also stayed relatively supportive. Institutional Property Advisors reported that Chicago apartment deliveries were expected to fall below 4,000 units for the first time since 2012, and CBD vacancy in 2025 hit its lowest level since at least 2006.

Cushman & Wakefield’s Q2 2025 report showed average effective rent of $3,029 per unit downtown with 94.7% occupancy. Still, renting is not friction-free. Zillow’s February 2026 rent report noted that Chicago metro asking rents were up 5.5% year over year, but 22.0% of rental listings were offering concessions.

Start With the Rental Math

The first question is simple: Will your condo truly cash flow? Many owners look at headline rent and assume holding is the better long-term move, but downtown condo ownership comes with costs that can narrow or erase the spread.

Using downtown averages, the market-level benchmark suggests roughly 8.2% gross annual rent before expenses, and about $34,400 in annual gross rent after a simple 5.3% vacancy assumption, based on the Cushman & Wakefield data. That can sound promising until you subtract the condo-specific costs that owners often underestimate.

Costs Owners Often Miss

Before you decide to keep the unit, look closely at:

- HOA dues

- Special assessments

- Property taxes

- Insurance

- Repairs and maintenance

- Vacancy periods

- Leasing fees or property management

- Mortgage payments, if applicable

In many downtown buildings, HOA dues are the factor that changes the entire picture. Even if your unit rents quickly, higher monthly assessments can leave you with weak or negative net cash flow once all expenses are included.

Think Net, Not Gross

That is why the better question is not, “What can I rent it for?” It is, “What is my net operating income after all condo-specific costs?”

If the monthly spread is thin, one unexpected repair, one assessment increase, or one vacant month can turn a decent-looking rental into a frustrating hold. In a condo market, the difference between a good rental and a poor one often comes down to building-level expenses rather than rent alone.

Property Taxes Can Shift the Equation

Property taxes deserve extra attention in Cook County. The Cook County Assessor noted that many Chicago homeowners could see higher tax burdens after the 2024 reassessment appeals cycle, and that 240,000 households had recently seen tax bills jump by 25% or more in a single year.

If you convert your condo to a rental, the tax side may also change because the homeowner exemption generally applies when you own and occupy the property as your principal residence. If you move out and lease the unit, you should assume your owner-occupied tax treatment may no longer apply.

That means your carry costs could rise even if rent stays steady. For many owners, this is the point where the hold strategy becomes less attractive than it first appeared.

The Tax Benefit of Selling Now

If this condo is still your primary residence, selling sooner may preserve a major tax advantage. The IRS home sale guidance says you can generally exclude up to $250,000 of gain, or $500,000 on a joint return, if you meet the ownership and use tests.

That exclusion can be one of the strongest reasons to sell instead of convert to a rental. Once a former primary residence becomes an investment property, the tax picture can become less favorable on a future sale.

Why Waiting Can Reduce the Exclusion

The IRS also notes that gain tied to periods of nonqualified use can be ineligible for the exclusion. In practical terms, that means turning your condo into a rental may reduce the tax benefit you could claim later.

Rental ownership also introduces depreciation. Under IRS Publication 925, residential rental property is generally depreciated over 27.5 years, and allowed or allowable depreciation affects your basis when you sell.

That surprises many owners. You may collect rent for several years, then discover the sale tax math is more complicated than expected because depreciation recapture changed your net outcome.

Selling Has Costs Too

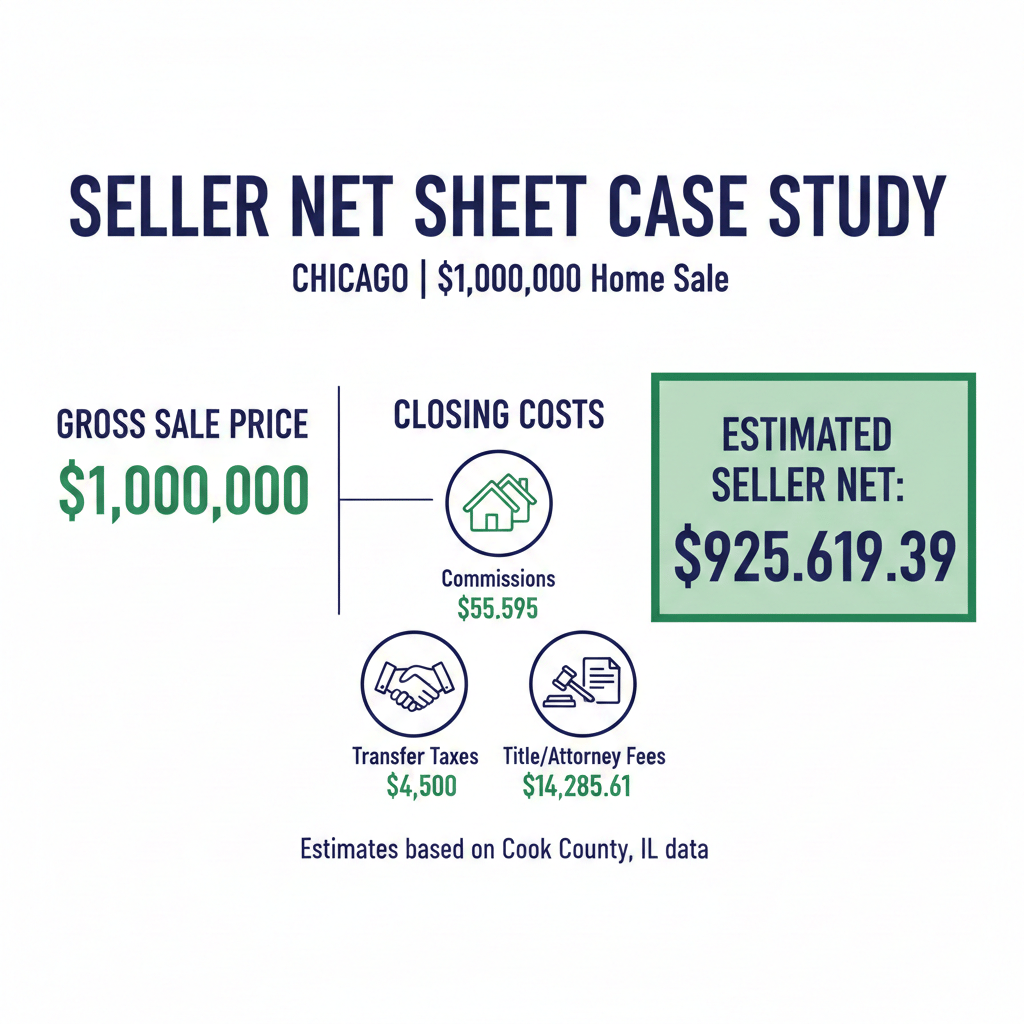

Of course, selling is not free. Chicago and Illinois transfer taxes reduce your net proceeds, so they should be part of your decision.

Under the City of Chicago code, the city real estate transfer tax is $3.75 per $500 of transfer price, plus a CTA supplemental tax of $1.50 per $500. Illinois also imposes a state transfer tax of 50 cents per $500, and Cook County imposes 25 cents per $500.

These costs do not automatically mean you should hold. They simply need to be weighed against your expected rental income, future tax exposure, and the time and responsibility that come with being a landlord.

Check Your HOA Before You Decide

One of the biggest mistakes condo owners make is assuming they are free to lease the unit. In Chicago, that answer is often building-specific.

Under the Illinois Condominium Property Act, condo governance flows through the recorded condominium instruments. In plain terms, you need to review your declaration, bylaws, and any leasing procedures before you count on a rental strategy.

Questions to Verify With Your Building

Before holding your condo as a rental, confirm:

- Whether leasing is allowed at all

- Whether there is a rental cap or waiting period

- What lease terms are permitted

- What fees, move-in charges, or approvals are required

- Whether your board requires specific lease paperwork or rider forms

This step matters more than many owners realize. A strong rent estimate does not help much if your building restricts leasing or adds enough friction to make the plan impractical.

Chicago Landlord Rules Are Real Work

If you keep the condo, you are not just holding an asset. You are stepping into a regulated rental environment.

The Chicago RLTO summary attached to the city lease form outlines several compliance duties for landlords. According to the 2026 Chicago Residential Lease materials, if you collect a security deposit, you must provide a receipt, hold it in a federally insured interest-bearing Illinois account, disclose the bank within 14 days, pay annual interest, provide an itemized damage statement within 30 days after move-out, and return the deposit within 45 days. The 2026 lease form lists the security-deposit interest rate at 0.01%.

For some owners, this is manageable. For others, especially if you are relocating or simply want a clean exit, this level of administration is a strong reason to sell instead.

When Selling Usually Makes More Sense

Selling is often the cleaner move when your condo no longer fits your life or your finances. It can also be the stronger financial choice if you want to protect equity and reduce complexity.

Selling may make more sense if:

- Your expected rent does not comfortably cover HOA dues, taxes, maintenance, and vacancy

- You want to preserve the home-sale exclusion

- Your building has restrictive leasing rules

- You would rather access your equity now

- You do not want the ongoing responsibilities of being a landlord

This logic fits the current market backdrop. Downtown sales remain active, and while rents are relatively supported, rental ownership is still more operationally and tax-wise complex than simply collecting a monthly check.

When Holding Can Be the Better Move

Keeping the condo as a rental can still make sense in the right situation. The strongest hold cases usually involve favorable financing, solid building economics, and a clear margin after all costs.

Holding may make more sense if:

- You have a low mortgage rate

- Your building allows leasing without major friction

- The unit can produce healthy cash flow after all expenses

- You want flexibility instead of selling immediately

- You are comfortable managing landlord duties or hiring help

The low new-supply backdrop downtown supports rent stability, based on the IPA forecast for Chicago multifamily. But appreciation should be viewed as selective, not automatic. Building quality, reserves, assessments, and micro-location still matter a great deal.

A Practical Way to Decide

If you are stuck between the two options, simplify the decision. Compare your likely net sale proceeds today with your likely true annual cash flow and future tax tradeoffs if you keep the condo.

A practical framework looks like this:

- Estimate your realistic sale price in your specific building.

- Subtract transfer taxes and other selling costs.

- Estimate realistic market rent for your exact unit.

- Subtract vacancy, HOA dues, taxes, insurance, maintenance, and management.

- Factor in whether losing the home-sale exclusion could hurt you later.

- Confirm your building’s leasing rules before moving forward.

For many downtown owners, the answer becomes clear once the numbers are laid out honestly. Sell if the equity and tax picture matter more than the monthly spread. Hold if the unit can genuinely cash flow after all condo-specific costs and you are comfortable acting as a landlord.

If you want a clearer picture of what your condo could sell for in today’s downtown market, Christine Hancock - Hancock Group can help you evaluate your building, pricing position, and likely net outcome with a seller-first strategy built around data, presentation, and local expertise.

FAQs

How much can I realistically rent my downtown Chicago condo for?

- Market averages provide a starting point, but your actual rent will depend on your building, layout, condition, view, amenities, and leasing competition. Downtown averages from Cushman & Wakefield showed $3,029 per unit in average effective rent, but your condo should be evaluated at the building level.

Will my downtown Chicago HOA allow me to lease my condo?

- You should verify your building’s declaration, bylaws, and leasing procedures before making plans. Some buildings allow leasing freely, while others may have rental caps, waiting periods, approval requirements, or lease term rules.

What happens to property taxes if I convert my Chicago condo into a rental?

- If the condo is no longer your principal residence, you should assume the owner-occupied homeowner exemption may no longer apply. That can increase your carrying costs, which is why tax changes should be part of your hold analysis.

If I rent out my former primary residence in Chicago, can I still use the home-sale exclusion later?

- Possibly, but the tax benefit may be reduced. IRS guidance says qualifying owners can generally exclude up to $250,000 of gain, or $500,000 on a joint return, but periods of nonqualified use can reduce the exclusion.

What transfer taxes apply when selling a downtown Chicago condo?

- Chicago currently imposes a city transfer tax of $3.75 per $500 of transfer price and a CTA supplemental tax of $1.50 per $500. Illinois also imposes 50 cents per $500, and Cook County imposes 25 cents per $500.