What makes a condo in Chicago’s West Loop a smart long-term play? You want a home you love in a neighborhood with staying power, and you also want to protect your money. This guide breaks down prices, rents, returns, building rules, and risks so you can decide with clarity. Let’s dive in.

West Loop market at a glance

The West Loop and Fulton Market corridor has transformed into one of Chicago’s most dynamic employment and dining hubs. Corporate and tech offices, award-winning restaurants, retail, and new hotels fuel steady housing demand. Recent reporting highlights Fulton Market’s rise as a prime address, which supports both resale values and rental interest over time. You can read more about the area’s momentum in Axios coverage of the Fulton Market corridor.

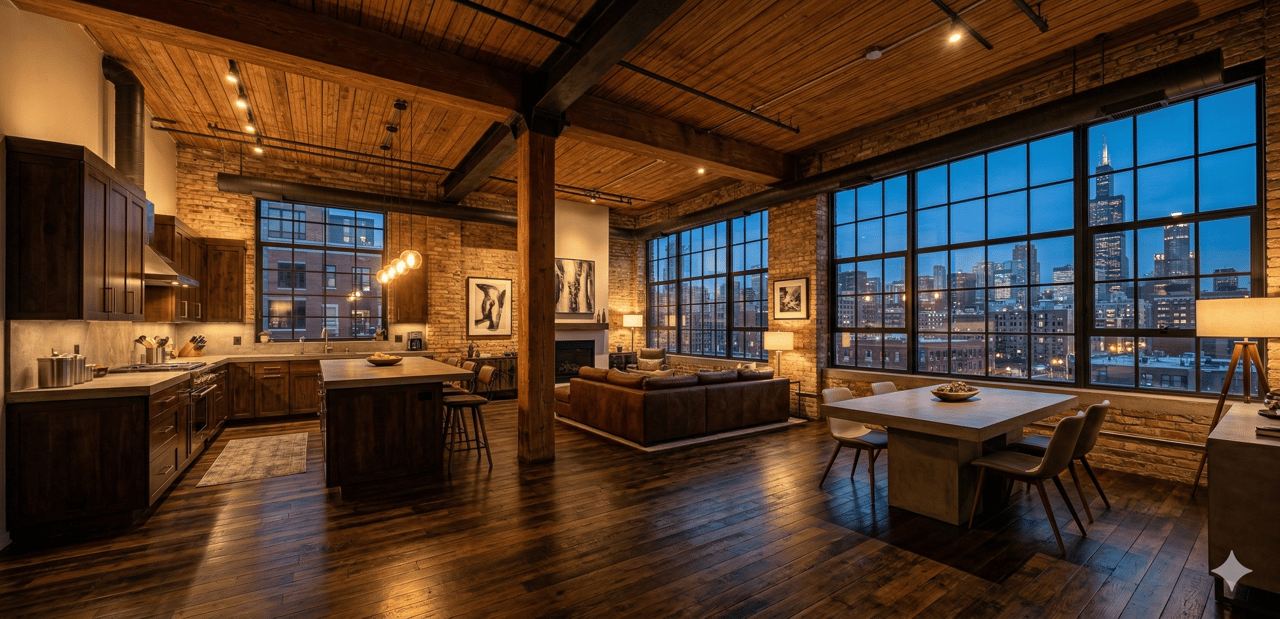

Median sale prices in the neighborhood often land around the mid-$400Ks to mid-$500Ks, depending on the data source and how the neighborhood is defined. That range reflects strong buyer demand and a varied mix of buildings, from classic lofts to newer luxury towers. As with any city neighborhood, unit-level details like floor plan, finishes, parking, and amenities drive value.

What rents and yields look like

Published trackers commonly show 1-bedroom asking rents in the West Loop in the roughly 2,200 to 3,000 dollar band. For example, RentCafe’s neighborhood snapshot has recent averages near 2,253 dollars, while other active-listing medians can read higher. Actual rent will vary by building, size, condition, view, and whether parking is included.

Here are two simple gross-yield examples to illustrate the math:

- Scenario A: Purchase price 535,000 dollars, monthly rent 2,286 dollars → annual rent ≈ 27,432 dollars → gross yield ≈ 5.1%.

- Scenario B: Purchase price 495,000 dollars, monthly rent 2,619 dollars → annual rent ≈ 31,428 dollars → gross yield ≈ 6.3%.

These examples show how typical West Loop condo gross yields often fall in a 4% to 7% range depending on the unit and data source. The exact return on your condo will depend on your purchase price, your building’s rentability, and how you manage costs.

The reality of net returns

After you factor in HOA dues, property taxes, insurance, management, and reserves for maintenance, a mid-5% gross yield can compress into a low single-digit net yield. That outcome is common for urban condos, where appreciation and resale demand often carry more of the total long-term return than pure cash flow.

- HOA dues: Many West Loop buildings fall in the 300 to 800 dollars per month range, and higher in full-amenity or luxury buildings. What dues cover varies, so review the budget and inclusions.

- Property taxes: Plan around Cook County’s effective property tax rates near 1.8% to 1.9% as a general planning reference. Use the county sites and tools like SmartAsset’s Illinois property tax calculator for estimates.

- Management, vacancy, and cap-ex: Full-service property management commonly runs about 8% to 12% of collected rent, with additional planning for vacancy and long-term repairs. See BiggerPockets’ overview of management costs for ballpark assumptions.

Rentability and tenant demand

The West Loop is renter-heavy compared with many neighborhoods. Published neighborhood and community-area snapshots often show owner-occupancy in the 25% to 35% range and renter-occupancy around 65% to 70% for the West Loop and Near West Side. That larger renter base supports leasing demand, especially near major employment nodes. You can explore neutral, data-driven demographics in Point2Homes’ West Loop overview.

High renter share can be a double-edged sword. It means a deep tenant pool, but it can also mean more buildings with leasing rules, rental caps, or investor concentration that affects financing for future buyers. That is why building-level due diligence matters as much as neighborhood averages.

HOA rules and financing you must know

Condo associations in Illinois can adopt leasing restrictions or rental caps if they follow their governing documents and the Illinois Condominium Property Act. If you plan to rent your unit now or later, confirm whether a cap exists, how the percentage is calculated, and how exceptions or waitlists work. For statutory context, see the Illinois Condominium Property Act. For a plain-language overview of how caps are implemented, this Hillcrest Management explainer is helpful.

Financing and warrantability also matter. Conventional and government-backed loans look at building health, including owner-occupancy, investor concentration, reserves, delinquencies, litigation, and single-entity ownership. A building that is non-warrantable can limit buyer financing options, which affects your future resale market. For a lender-style summary of approval criteria, review this condominium approval guideline reference.

Supply, new construction, and appreciation

West Loop and Fulton Market have seen years of new office, residential, and mixed-use development, including luxury condo deliveries. New supply can soften near-term pricing or rent growth within specific segments. Over a longer horizon, the area’s employment base and amenity set continue to underpin demand. For neighborhood context, see Axios’ reporting on Fulton Market’s growth.

Your takeaway: track the micro-market. Compare current inventory, absorption, and concessions in your building’s tier before projecting appreciation.

Due-diligence checklist for West Loop condos

Before you buy, or before you decide to hold and rent, work through this list to protect your downside and keep your options open:

-

Governing documents. Read the declaration, bylaws, and rules for any rental restrictions, waitlists, minimum owner-occupancy periods, short-term rental bans, and how amendments are adopted. The Hillcrest overview of rental caps explains common approaches.

-

Owner-occupancy and percent rented. Ask the association for an up-to-date count. Some public datasets can offer community-area context. For a broader Near West Side lens, review the Institute for Housing Studies data portal.

-

HOA budget, reserves, and minutes. Look for a balanced budget, a reasonable reserve allocation, and any recent or pending special assessments. Fannie Mae and many lenders view adequate reserves as a marker of building health. For lending context, see the condo approval guideline reference.

-

Delinquencies and litigation. Request the percent of owners more than 60 days delinquent and disclosures on any pending litigation. These issues can limit buyer financing at resale.

-

Master insurance and deductibles. Confirm what the master policy covers versus your HO-6, and the size of deductibles that could trigger owner costs or special assessments.

-

Parking and storage. In-city renters often pay a premium for a deeded or assigned parking space. Lack of parking can impact rentability and resale.

-

Current rental comps and concessions. Pull 3 to 5 active comps in the same building or on the same block and note any concessions. Seasonality matters. Neighborhood trackers like RentCafe help you frame expectations.

-

Financing and warrantability. Have a lender review the building early. Knowing whether conventional, FHA, or VA financing is viable will tell you a lot about your future buyer pool. The condo approval reference outlines common tests.

Who a West Loop condo fits best

A West Loop condo can be a smart long-term hold if you:

- Value walkability, dining, and fast access to employment centers like Fulton Market.

- Plan to live in the unit first and rent later, or you are a selective investor who underwrites conservatively.

- Choose a building with solid reserves, reasonable dues, and a rental policy that preserves future flexibility and financing options.

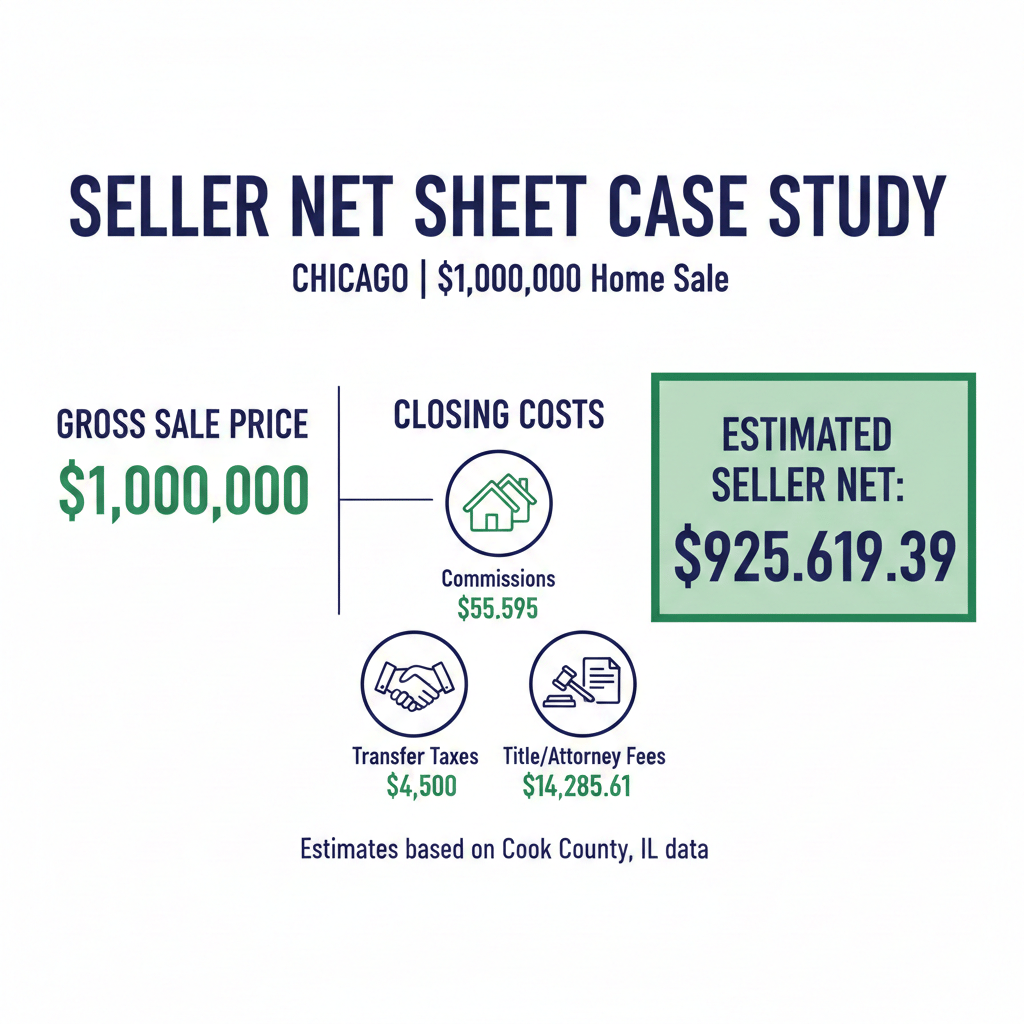

If you are a pure cash-flow investor seeking high immediate yields, proceed with caution. After HOA dues, taxes, management, and reserves, many West Loop condos produce modest cash-on-cash returns. In that case, your thesis should lean more on long-term neighborhood appeal and selective buying under market value than on short-term income.

Should you rent or sell your West Loop condo?

If you already own in the West Loop, you have two strong paths. Renting can make sense if your building allows it, your net yield pencils out, and you want to hold for appreciation. Selling can be the better move if your unit commands a premium today, your HOA or financing profile limits future liquidity, or you prefer to redeploy equity elsewhere.

If you are considering a sale, presentation and pricing precision are everything. Professional marketing, staging, and building-level positioning can meaningfully raise your net. If you are weighing a buy-and-hold, building-level analysis and conservative underwriting will protect your downside and preserve exit options later.

FAQs

What are typical West Loop 1-bedroom rents today?

- Neighborhood trackers often show 1-bedroom asking rents in the 2,200 to 3,000 dollar range, with RentCafe’s recent average near 2,253 dollars.

How do HOA dues affect condo investment returns in West Loop?

- Dues commonly range from about 300 to 800 dollars per month in many buildings, which can reduce net yield several points once combined with taxes, insurance, management, vacancy, and reserves.

Can my West Loop condo association limit rentals?

- Yes. Associations can adopt rental caps or leasing rules if they follow governing documents and state law. Review your documents and the Illinois Condominium Property Act.

Why does building “warrantability” matter for resale?

- Lenders consider owner-occupancy, reserves, delinquencies, litigation, and investor concentration. If a building is non-warrantable, buyer financing can be limited, shrinking your potential buyer pool. See this condo approval guideline reference.

Is the West Loop more renter- or owner-oriented?

- Data snapshots often show a renter majority in the West Loop and Near West Side, which supports leasing demand. For neutral context, see Point2Homes’ West Loop demographics.

ABOUT THE AUTHOR

Christine Hancock is a Chicago Realtor with @properties Christie’s International Real Estate and brings more than 25 years of experience in the downtown Chicago condo market. She specializes in high-rise and luxury condominium sales in West Loop, South Loop, River North, and Streeterville, helping buyers and sellers navigate complex transactions with data-driven pricing strategies and in-depth neighborhood expertise.

Christine works with both buyers and sellers to evaluate market trends, position properties competitively, and make confident real estate decisions in Chicago’s dynamic downtown housing market.

Call or text 312-296-9300 to discuss current market conditions or your real estate plans.