You Don't Need 20% Down to Buy a Home in Chicago

Do you really need 20% down to buy a home? No. Most buyers put down far less, and some programs require nothing at all.

The Short Answer

The average down payment for first-time homebuyers is around 6%, not 20%. Dozens of loan programs exist with down payments as low as 0% to 3.5%. Meeting with a lender before you start shopping is the single most important step you can take.

Where Did the 20% Rule Come From?

It's a myth that won't die.

The 20% down idea came from conventional mortgage guidelines that let you avoid private mortgage insurance (PMI). That's it. It was never a requirement. It was never a rule. It was a threshold to skip one fee.

And yet buyers have been delaying homeownership for years because of it.

Don't let a number that doesn't apply to you stop you from buying.

What Do Buyers Actually Put Down?

Here's the reality. Most people are not putting 20% down.

According to the National Association of Realtors, the median down payment for first-time homebuyers is around 6%. Repeat buyers come in closer to 17%, and that includes buyers who used equity from a previous sale.

The 20% benchmark is not the norm. It never was.

What Loan Programs Are Available?

There are more options than most buyers realize. Here's a quick breakdown:

FHA Loans Down payments as low as 3.5%. Flexible credit requirements. One of the most popular options for first-time buyers. Learn more at HUD.gov.

Conventional Loans (Fannie Mae / Freddie Mac) Down payments as low as 3% for qualified buyers. Good option if you have solid credit and steady income.

VA Loans 0% down for eligible veterans and active-duty service members. No PMI. One of the strongest mortgage products available. Details at VA.gov.

USDA Loans 0% down for properties in qualifying rural and some suburban areas. Income limits apply.

Illinois-Specific Programs The Illinois Housing Development Authority (IHDA) offers down payment assistance, closing cost grants, and reduced-rate mortgages for Illinois buyers. These programs are frequently underused because buyers don't know they exist.

Why You Should Talk to a Lender First

Most buyers start by browsing Zillow. That's backwards.

Before you look at a single listing, you need to know:

- How much you're actually approved for

- Which loan programs you qualify for

- How much cash you'll need at closing

- What your monthly payment looks like at different price points

A lender pre-approval does all of that. It takes 30 to 60 minutes. It costs nothing. And it changes everything about how you search.

In Chicago's downtown condo market, including neighborhoods like West Loop, River North, South Loop, and Streeterville, well-priced units move fast. Sellers want buyers who are already approved, not buyers still figuring out their finances.

By the time you're ready to look, you should already know your number.

What About PMI?

Private mortgage insurance (PMI) is often cited as the reason to put 20% down. Here's what to know.

PMI is typically 0.5% to 1.5% of your loan amount per year. On a $400,000 loan, that's roughly $166 to $500 per month. That's real money.

But here's the math people miss: if you're waiting years to save 20% while Chicago home prices rise, you may be losing more in appreciation than you're saving on PMI. A lender can model both scenarios for you. That's why the conversation happens before you start looking, not after.

According to Redfin, Chicago home prices have shown consistent appreciation across downtown neighborhoods over the past several years. Waiting costs money too.

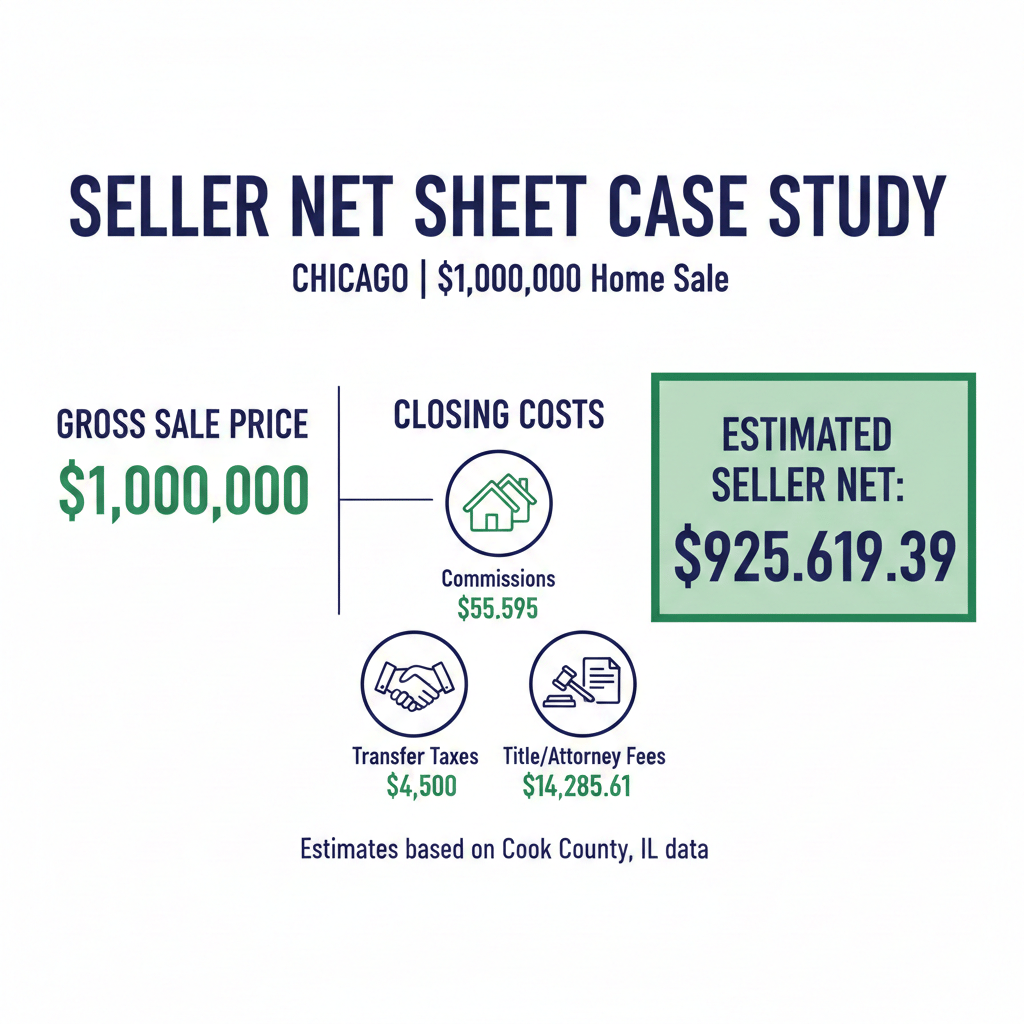

How Much Cash Do You Actually Need?

Down payment is only part of it. Plan for these costs:

- Down payment: 0% to 20% depending on loan type

- Closing costs: typically 2% to 5% of the purchase price

- Earnest money: usually 1% to 2%, applied toward closing

- Home inspection: $300 to $600 for a condo

- Reserve funds: some condo buildings require proof of reserves post-close

A lender will walk you through all of this in your first conversation. No surprises.

Downtown Chicago Condos and Down Payments

One more thing worth knowing if you're buying in Downtown Chicago.

Some condo buildings have HOA guidelines that affect financing. Certain high-rise buildings are not approved for FHA or VA loans due to their owner-occupancy ratios or reserve fund levels. That means the type of loan you can use depends partly on which building you're buying in.

This is something I know well. I've closed over 300 sales in the West Loop alone, including 86 units at 125 S. Jefferson. I know which buildings are FHA-approved, which are not, and how that affects your financing options before you ever make an offer.

That's the kind of local knowledge that saves you from falling in love with a unit you can't finance.

Key Takeaways

- The average first-time buyer puts down around 6%, not 20%

- Programs like FHA, VA, USDA, and IHDA offer down payments as low as 0%

- A lender pre-approval is step one, before you look at a single listing

- PMI is a cost, but it is not always a reason to delay buying

- In Downtown Chicago, some buildings have financing restrictions. Know before you look.

Bottom Line

You don't need 20% down. You need a plan.

That plan starts with a 30-minute conversation with a lender. Once you know what you qualify for, what your down payment looks like, and what your monthly payment will be, buying a home stops feeling out of reach. It starts feeling like a real next step.

If you're thinking about buying a condo in West Loop, River North, South Loop, Streeterville, or anywhere else in Downtown Chicago, let's talk. I can connect you with trusted lenders who know this market, and I can help you figure out exactly what to look for once you're ready.

FAQ

How much do I really need for a down payment in Chicago? It depends on the loan program. FHA requires 3.5%, conventional loans can start at 3%, and VA and USDA loans offer 0% down for qualifying buyers. The Illinois Housing Development Authority also has down payment assistance programs for Illinois residents.

What is PMI and do I have to pay it? PMI is private mortgage insurance required when you put less than 20% down on a conventional loan. It typically costs 0.5% to 1.5% of your loan amount annually. It can be removed once you reach 20% equity in your home.

Should I get pre-approved before looking at condos in Chicago? Yes. Pre-approval tells you what you can afford, which loan programs you qualify for, and signals to sellers that you're a serious buyer. In a fast-moving market like Downtown Chicago, it's a requirement, not a suggestion.

Are all downtown Chicago condos eligible for FHA loans? No. FHA and VA loans have building-level approval requirements. Some high-rise buildings in Chicago do not qualify due to owner-occupancy ratios or HOA financials. Working with an experienced condo specialist helps you avoid financing surprises.

What other costs should I budget for beyond the down payment? Plan for closing costs of 2% to 5% of the purchase price, earnest money of 1% to 2%, inspection fees, and potential post-closing reserve requirements from your condo association.

Call or text Christine Hancock at 312-296-9300 to talk about buying a condo in Downtown Chicago, or to get connected with a lender who knows this market.

ABOUT THE AUTHOR

Christine Hancock is a Chicago Realtor with @properties Christie's International Real Estate, bringing more than 25 years of experience and over $200 million in closed sales in the downtown condo market. With 96 five-star Zillow reviews, Christine is recognized for her commitment to client satisfaction and market expertise.

She specializes in high-rise and luxury condominium sales in West Loop, South Loop, River North, and Streeterville, helping buyers and sellers navigate complex transactions with data-driven pricing strategies and deep neighborhood insight.

Christine partners with clients to evaluate market trends, position properties competitively, and make confident, informed decisions in Chicago's vibrant downtown housing market.

Call or text 312-296-9300 to discuss current market conditions or your real estate goals.