How to Read a Chicago Condo Reserve Fund Study Before You Buy

You found the one. Price works. Location is right. But you haven't looked at the reserve fund study yet. Most buyers skip it. Big mistake.

THE SHORT ANSWER

A reserve fund study is an engineering-based report that tells you whether a condo building has enough money saved to cover future major repairs. In Chicago's downtown condo market, an underfunded reserve is one of the most common causes of unexpected special assessments. Reading this document before you buy is one of the smartest moves you can make.

What Is a Reserve Fund Study?

It's a formal analysis of the building's major physical components, what they cost to replace, and how long they have left.

An engineer or reserve specialist inspects the property and catalogs big-ticket items: roofs, elevators, boilers, HVAC systems, windows, façades, parking structures, and common area finishes. For each one, the report estimates remaining useful life and replacement cost.

From that data, the association gets a recommended funding plan. The study tells the board how much money they should have saved today, and how much they need to be adding each year.

In Illinois, condo associations are required to maintain reserves, but they are not legally required to be fully funded. That gap is where buyers get hurt.

Why Does This Matter for Downtown Chicago Buyers?

Chicago's downtown condo inventory includes buildings of every age, from converted lofts in the West Loop that date back 100 years to glass towers in River North that went up a decade ago. Age and complexity drive reserve needs dramatically.

An older West Loop loft conversion might be sitting on aging plumbing, a flat roof near end of life, and original elevators. A newer Streeterville high-rise might have pristine infrastructure but a brand-new reserve fund that hasn't had time to build up. Neither situation is automatically a dealbreaker. But you need to know what you're walking into.

When buildings don't have enough reserves and a major repair comes due, the association has two options: take out a loan, or charge every owner a special assessment. Neither is fun.

According to the Community Associations Institute, underfunded reserves are among the leading causes of unexpected financial hardship for condo owners nationwide. In dense urban markets like Chicago, where buildings have more complex systems, the risk is amplified.

What Does "Percent Funded" Actually Mean?

This is the number you're hunting for. Every reserve study includes a percent funded figure.

It compares how much money the association currently has saved to how much the study says they should have saved right now, based on component ages and replacement costs.

Here's a simple way to think about it:

- 70% funded or above = healthy. The building is staying ahead of its obligations.

- 30% to 70% funded = watch closely. Manageable, but ask follow-up questions about the funding plan.

- Below 30% funded = red flag. This building may not have enough to cover major repairs without special assessments.

The National Association of Realtors and most reserve planning professionals use 70% as the general benchmark for a well-funded association.

A building at 15% funded isn't just underfunded. It's behind. If the elevator needs replacement in two years and there's no money saved, guess who pays? Every unit owner, including you.

What Does Underfunded Look Like in a Real Document?

You're looking at a table or spreadsheet that lists each major component. Here's what to pay attention to:

Remaining useful life. If multiple components show 1 to 5 years of useful life remaining and the reserve is underfunded, that's a combination that signals near-term assessments.

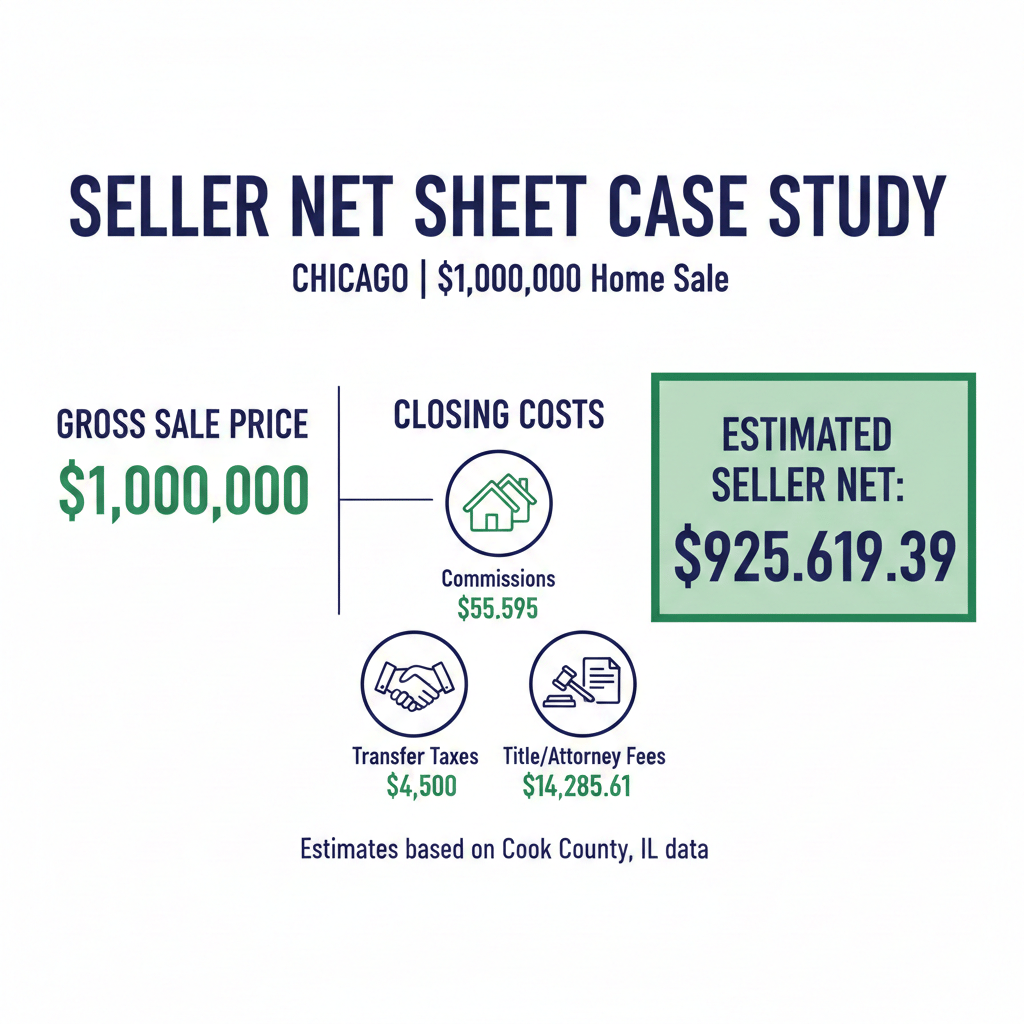

Fully funded balance vs. actual balance. See the gap between what they should have and what they actually have. A $400,000 shortfall in a 200-unit building? That's $2,000 per unit. Spread over two years, you're writing a check you didn't plan for.

Annual contribution. The study recommends how much the association should contribute annually. If the current budget is far below that number, the board is underfunding reserves and kicking the problem down the road.

The funding plan projection. Most studies include a 20 to 30-year projection. A well-managed building's projection trends upward. An underfunded building's projection often shows deficits in the near-term years.

How Do You Get the Reserve Study Before You Buy?

In Illinois, sellers are required to provide a 22.1 disclosure package to buyers. This package includes the reserve study, the association's most recent budget, meeting minutes, and other financial disclosures.

Request it early. The moment you're serious about a unit, ask for the 22.1 package. Don't wait until after attorney review starts.

Once you have it, look for the reserve study date. A study more than three years old may not reflect current component conditions or costs. If the association hasn't updated it recently, that itself is a signal about how the board operates.

Downtown Chicago buildings in the West Loop, River North, Gold Coast, and South Loop all handle reserves differently. Some boards are proactive and conservative. Others defer until a problem forces action. The study tells you which kind of board you're dealing with.

What Questions Should You Ask After Reading the Reserve Study?

Don't stop at the document. Use what you find to ask direct questions:

- What is the current percent funded?

- When was the reserve study last updated?

- Is the association currently meeting the recommended annual contribution?

- Are any major projects, like roof, elevator, or boiler replacement, anticipated in the next 3 to 5 years?

- Have there been special assessments in the last five years, and are any being discussed now?

A seller or listing agent who can't answer these questions is a signal. A board that won't share the documents is a bigger one.

According to Redfin's buyer guidance on condo due diligence, reviewing HOA financials, including reserve studies, is a critical step buyers often skip under time pressure. Don't let urgency override diligence.

What Do Healthy Reserves Look Like in Downtown Chicago Buildings?

In my experience working with buyers across 300+ West Loop transactions and across neighborhoods including River North, Streeterville, and South Loop, the best-run buildings share a few traits.

They update their reserve study every three to five years. They fund at or above the recommended annual contribution. Their board meeting minutes reflect proactive conversations about upcoming capital needs, not reactive scrambling after something breaks.

A building at 1000 W. Washington Blvd. or 900 W. Washington Blvd. that has maintained strong reserves over time is a very different investment than a similarly priced unit in a building that's been chronically underfunding for a decade.

The number on the page tells the story. Learn to read it.

Key Takeaways

- A reserve fund study shows whether a condo building has enough money saved for future major repairs.

- Look for the percent funded figure: 70% or above is considered healthy, below 30% is a red flag.

- Request the 22.1 disclosure package early in your search, before attorney review begins.

- Check the remaining useful life of major components against the funded balance.

- A low percent funded number with aging infrastructure is a strong signal of upcoming special assessments.

The Bottom Line

The price tag on a Chicago condo doesn't tell the whole story. The reserve fund study does.

A building with an underfunded reserve and aging systems is a liability that doesn't show up in the listing. But it will show up on your bank statement. Possibly more than once.

Before you fall in love with a floor plan, fall in love with the financials. If the reserve study is healthy, you're buying into a well-managed building. If it's not, at minimum you know what you're negotiating. That knowledge is what separates smart buyers from surprised ones.

Ready to dig into the financials on a specific building? Call or text Christine Hancock at 312-296-9300 to talk through what the numbers say and whether the building is worth your offer.

FAQ

What is a condo reserve fund study? A reserve fund study is an engineering analysis of a condo building's major components, their remaining useful life, and the cost to replace them. It tells buyers and the association how much money should be saved and whether the building is on track.

What percent funded is good for a condo association in Chicago? Most reserve planning professionals and the National Association of Realtors consider 70% funded or above to be healthy. Below 30% funded is considered underfunded and signals a higher risk of special assessments.

Can I get the reserve study before making an offer in Illinois? Yes. Illinois law requires sellers to provide a 22.1 disclosure package, which includes the reserve study, current budget, and meeting minutes. Request it as soon as you're serious about a unit.

What happens if a Chicago condo building is underfunded? When major repairs come due and reserves are insufficient, the association typically charges owners a special assessment or takes out a loan. Both outcomes increase your cost of ownership beyond your monthly HOA fee.

Does the age of the reserve study matter? Yes. A study more than three years old may not reflect current repair costs or component conditions. Ask when the last study was done and whether the association is meeting the recommended annual contribution.

ABOUT THE AUTHOR

Christine Hancock is a Chicago Realtor with @properties Christie's International Real Estate, bringing more than 25 years of experience and over $200 million in closed sales in the downtown condo market. With 96 five-star Zillow reviews, Christine is recognized for her commitment to client satisfaction and market expertise.

She specializes in high-rise and luxury condominium sales in West Loop, South Loop, River North, and Streeterville, helping buyers and sellers navigate complex transactions with data-driven pricing strategies and deep neighborhood insight.

Christine partners with clients to evaluate market trends, position properties competitively, and make confident, informed decisions in Chicago's vibrant downtown housing market.

Call or text 312-296-9300 to discuss current market conditions or your real estate goals.